Quote:

Originally Posted by suburbanite

So interest rates are the biggest determinant of prices, and Americans could previously lock in 2% rates. Chicago also has higher median incomes than Toronto. In theory we should be able to go back and see Chicagoans bidding up all the supply in Chicago and actually reaching real prices in excess of what Toronto saw during 2020-2022. All that matters is that they basically had the ability to lock in free money for the entirety of their 30 year mortgage right?

I'd love to see the graph for that. Or maybe, just maybe, Chicago actually has a relatively healthy balance of supply and demand and so people don't unnecessarily bid up assets and overindebt themselves when there isn't the level of competition to necessitate it.

|

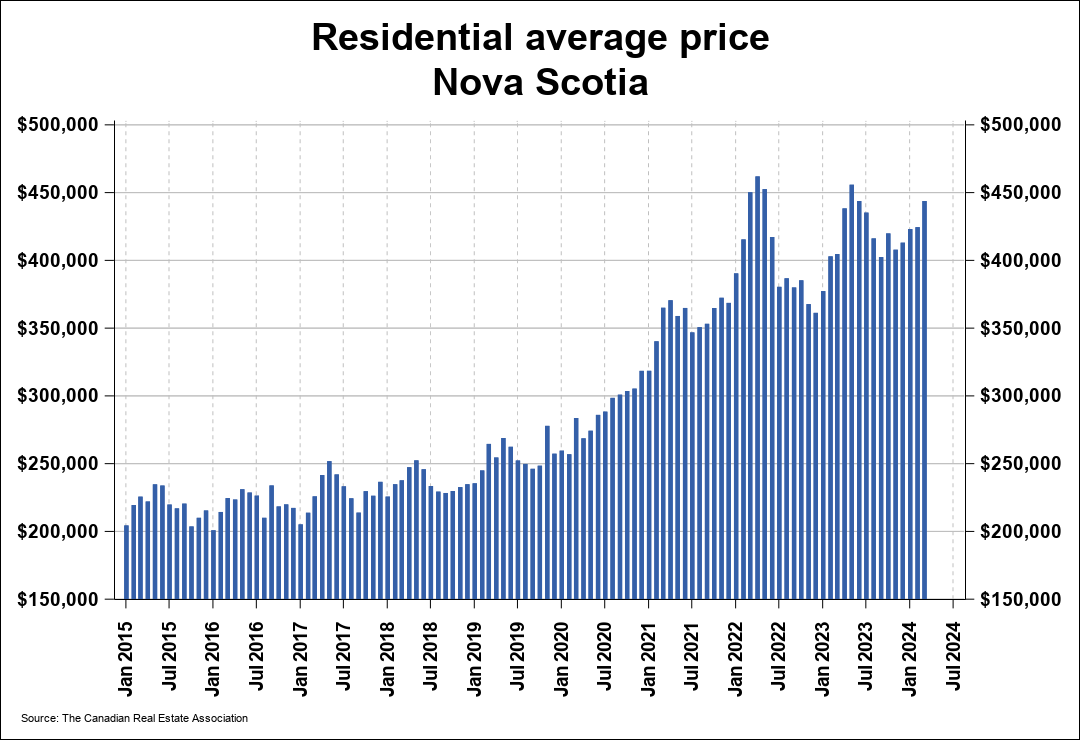

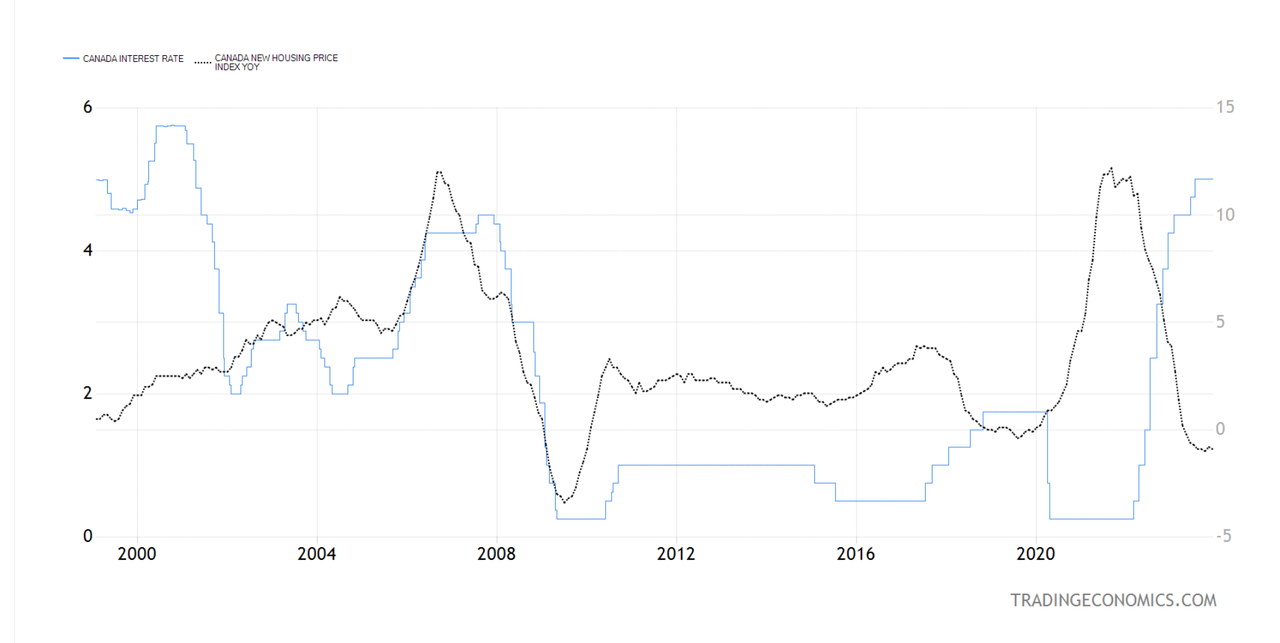

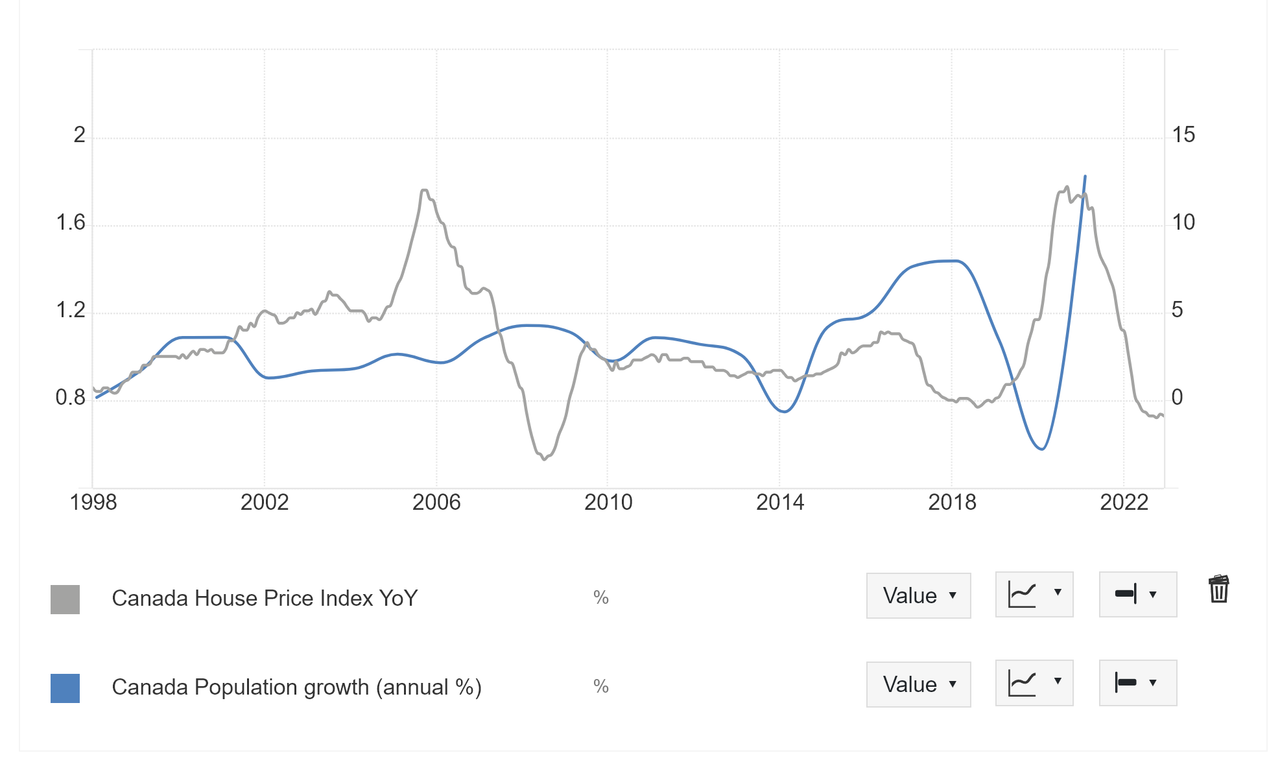

My argument is about impact of interest rates in the Canadian market only. Unlike in the US, where interest rates only affect a small fraction of homebuyers, in Canada, these rates have a more immediate and significant effect on house prices. This is evident in the current scenario where, despite an increase in rates in the US, house prices have risen by 6.3 percent year-on-year in Chicago, even amidst a declining population. In contrast, prices are falling in Toronto, a city experiencing high population growth.

https://www.fhfa.gov/AboutUs/Reports...October%202023.

In the US, the fixed 30-year mortgages, which were recently low for most people, coupled with the current high rates, discourages homeowners from selling. They would have to buy a new house with much higher interest rates. This reluctance to sell reduces supply or inventory, leading to an increase in house prices. In Canada, whether homeowners sell or not, they are still affected by higher rates. Consequently, people continue to list properties, increasing supply and causing prices to fall, as seen in Toronto.

Therefore, the dynamics between interest rates in Canada and the US are much different. In Canada, interest rates have a more substantial effect than factors like immigration or population growth.

So prices rise and fall faster in Canada than the US based on high or low interest rate.

Prev

Prev

Linear Mode

Linear Mode