Quote:

Originally Posted by whatnext

That may be but the overall market is struggling as well. That’s going to make it hard to convince developers to build when we apparently need a lot of housing. As I’ve said government policies have backed us into a place where the housing people need apparently can’t be built at a price they can afford.

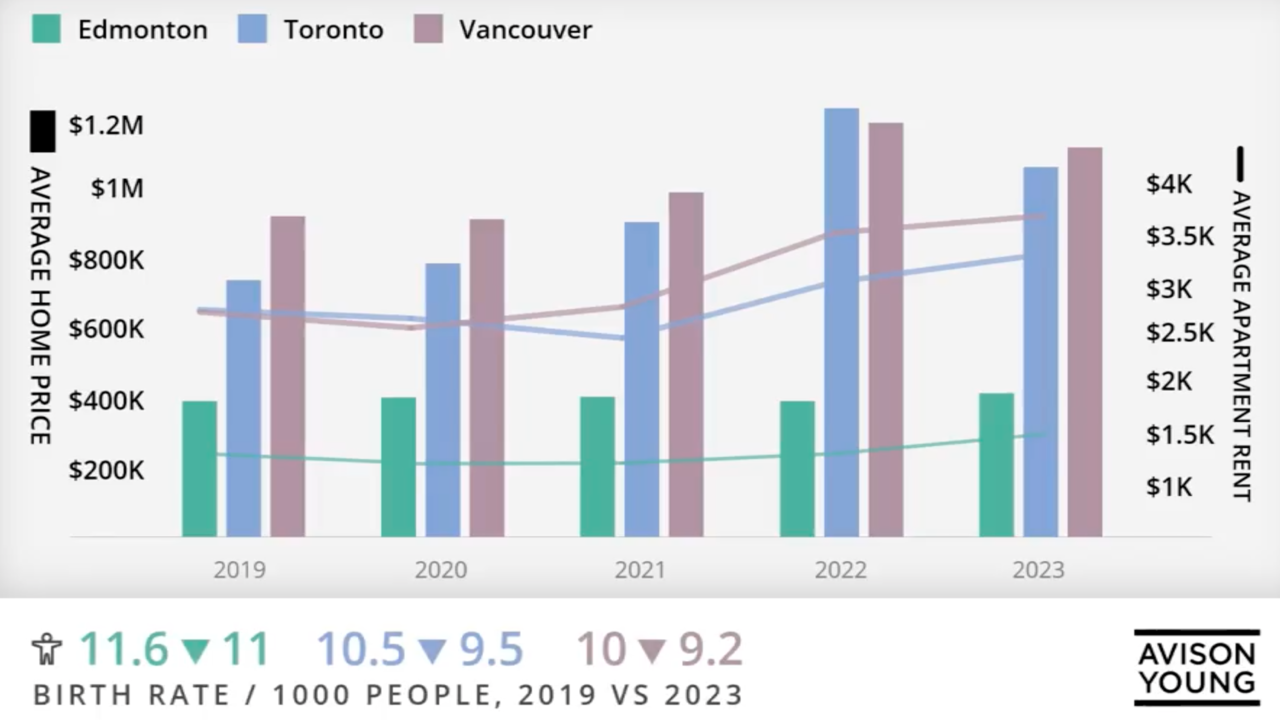

Rate Cut Not Enough To Spark Fraser Valley Market Activity In June

Inventory in the Fraser Valley has continued to build up for the sixth straight month while home sales remain soft.

Those who were hoping the Bank of Canada's rate cut on June 5 would spark activity in the real estate market will have to continue waiting, as home sales in the Fraser Valley went the other direction in June, according to statistics published by the Fraser Valley Real Estate Board (FVREB) on Wednesday.

In June, the Fraser Valley recorded a grand total of 1,317 home sales, which represents a decrease of 13% from May 2024 and a decrease of over 30% from both this time last year and the 10-year average for June.….

https://storeys.com/fraser-valley-re...ate-june-2024/ |

In expensive markets (Toronto, Vancouver, Fraser Valley etc) affordability is very limited. What you're seeing is sales numbers below 10 year average (in the Fraser Valley and in the new Vancouver monthly data), and the number of homes on the market rising. Yet prices are still only falling slightly (they're up 0.5% year-on-year in Vancouver, so a slight drop, allowing for inflation).

It'll take many more years of steady price drops (or lower interest rates) for prices to fall to more affordable levels. Blaming 'the government' is easy, but the government didn't buy all the homes at ever-increasing prices, that it turns out aren't as good an investment as the buyers thought, or they can't really afford now interest rates are higher (but by no means high in historical sense). People - almost all Canadian people - borrowed more than they should because of a series of myths, or lies they told themselves. 'Interest rates can't go up', 'prices never go down', 'they'll never close down AirBnB'.

Institutions haven't helped - Candian Banks, and 'alternative lenders' have loaned far more than they would have years ago, and you can argue the government should have regulated them more tightly (but it's supposed to be a free country where people can make their own decisions). The Bank of Canada could have kept interest rates a little higher, (but their main job is to avoid out of control inflation, while avoiding recessions). And obviously recent immigration levels (especially of overseas students) have helped keep prices up in some markets by creating more demand.

People's buying decisions having created the problem, they are also the solution. That's what you're seeing now. They're not buying, and sellers are reluctantly lowering their prices (or walking away, leaving the lenders to clear up the mess with a foreclosure sale). "transaction-level data do show that well-priced properties are still selling quickly, suggesting astute buyers are able to spot value and act when opportunities arise.” [

REBGV June report] Home prices can rise like a rocket, but they usually take a lot longer to come back down again, (and if they come down as fast as they went up, there's a serious economic impact).

Developers who only build to sell will slow, or stop building, and those who bought land on credit will fail. Bigger builders, or more nimble ones, will switch to rentals, because the demand for homes still exists. (Westbank just applied to build 3 rental towers with nearly 1,000 units in the Downtown Eastside, for example).

There's no easy, or instant fix, and there will be casualties, just as there have been every time the market gets overextended.

Prev

Prev

Linear Mode

Linear Mode