Quote:

Originally Posted by 10023

The Undershaft building is a disaster and it would be a shame if that became the tallest building in London.

Limehouse and Shadwell (and Stepney) would be good places to see more tower developments, perhaps even eventually linking the City with Canary Wharf with a sort of loose linear skyline. There's certainly enough postwar architecture around that could be redeveloped without anyone missing it. The problem would be transportation... in retrospect the DLR should have been heavy rail.

|

There is certainly scope to redevelop large swathes of the 'Blitz' post-war estates located in-between the City and Canary Wharf; a couple of 100m+ towers, and intensification of mansion blocks, but we won't see a sprawling skyline develop between the two. What is more likely is for a 100m+ skyline to emerge around Whitechapel, and subsequently merge with the cluster around Aldgate, but again protected sight-lines will restrict anything of any notable height.

It is all very good speculating that the DLR ought to have been heavy-rail from the beginning, but it probably would never have received funding had that been the case. You have to remember that most of the London Docklands was a basket case; it even stood in for Huế in Stanley Kubrick's

Full Metal Jacket. Had the DLR been a heavy rail line, it would not have developed into the sprawling six-line network that it is today serving a very large number of regeneration zones, nor would it have had the large number of interchanges that increase passenger mobility in east London.

The DLR was a low-cost catalyst that unlocked far more regeneration than originally envisioned. Without the DLR, we would never have got the Jubilee Line extension to Canary Wharf and Stratford, and subsequently Crossrail 1.

Quote:

Originally Posted by 10023

|

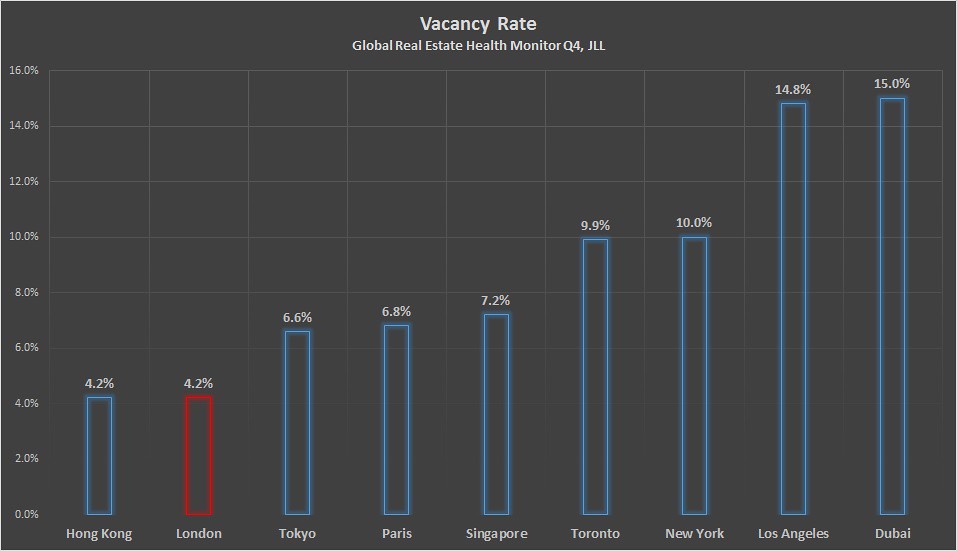

Granted, following the referendum there is more uncertainty in the market, but you are obfuscating the sector outlook when the fundamental issue with property in London and the UK is the lack of supply that predates the referendum outcome by several decades. It is for that reason why housing has become so expensive, and why office vacancy rates are so low relative to other international cities.

Source:

http://www.jll.com/Research/Global-M...2-42219ec19bf0

There have been concerns over recent months about the super-prime residential sub-sector, where the pipeline has become distorted, but the rest of the market needs more units, not less, and thus we will likely see a shift towards more mainstream units in the coming months and years. To put this entire situation into context, I noticed on another thread, (admittedly long-term) projections for New York's population reaching 9mn by 2040.

London is expected to surpass that figure in the next three years.

On a side note, AXA have since announced that they are progressing with the Pinnacle project (the focus of the FT article you refer to) which comes as no surprise considering that demand for office space in London.